Before I start, I hope this finds you well. I know that there are clients who have found themselves on the unfortunate end of the consequences of the Corona Virus either economically or in health. Nobody deserves this but we will get through it, so I hope you remain positive and safe. It goes without saying anyone who has been financially affected and is looking for some for financial advice at this time can contact me directly: robert@rockwellfinancial.ie

I felt it was time to send you something on what’s happening in the Financial Markets, how it’s affecting your portfolios’ and more importantly some advice on what to do from here. I promise this will be concise and free of all investment jargon, but I hope I gives you some reassurances in this turbulent time.

If you are the type to stop reading here as newsletters aren’t your thing then here’s the summary:

Markets are volatile right now. No one has a clue where the bottom is (well history has some pointers, but you’ll have to read on further to see that!) so the last thing to do is switch to cash at this juncture. It’ll turn. It always does. Your portfolio has been designed to make sure it’s invested in a diverse range of assets. This is what will insulate you as an investor. We didn’t put ‘all your eggs in one basket’ for a reason and now is the time to reap that dividend. You are not invested in 100% of equities unless you specially said you wanted to be and could tolerate the type of volatility we are now seeing.

Either way, the best advice from here is to simply do nothing as you’ll only crystallise the bad performance. If you do have disposable cash, have the stomach for more volatility and can afford to increase your monthly contribution, then there has never been a better time to do so. If you don’t then that’s perfectly fine. It’s easy for me to say such things but it’s your money and as we always say, you can only save what you can afford to save for as long as you can afford to save it!

1.) So, what’s happening in the markets?

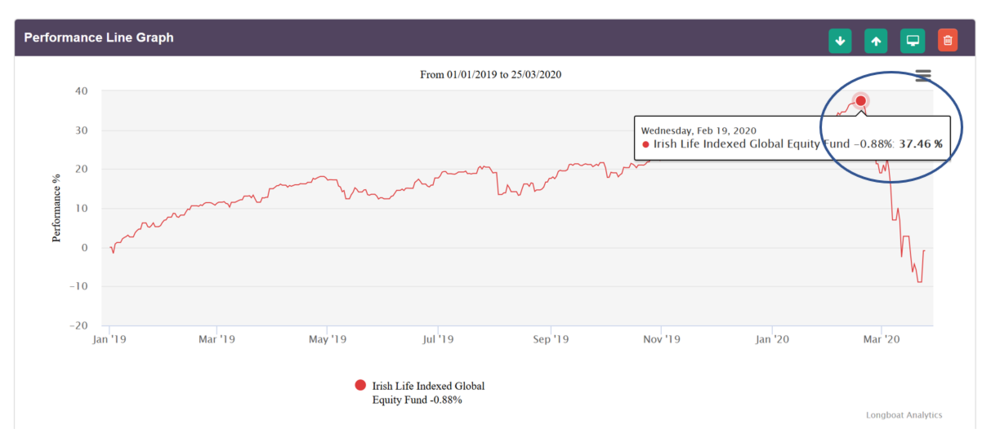

It is also worth highlighting that we had a record year in 2019 which added fuel to the fire, and can part explain the sudden ‘sell off’ as people were simply profit taking. (see Chart B)

Chart B. Global Stock Market Performance 01/01/2019 to 25/03/2020

2.) What does this mean for your Portfolio?

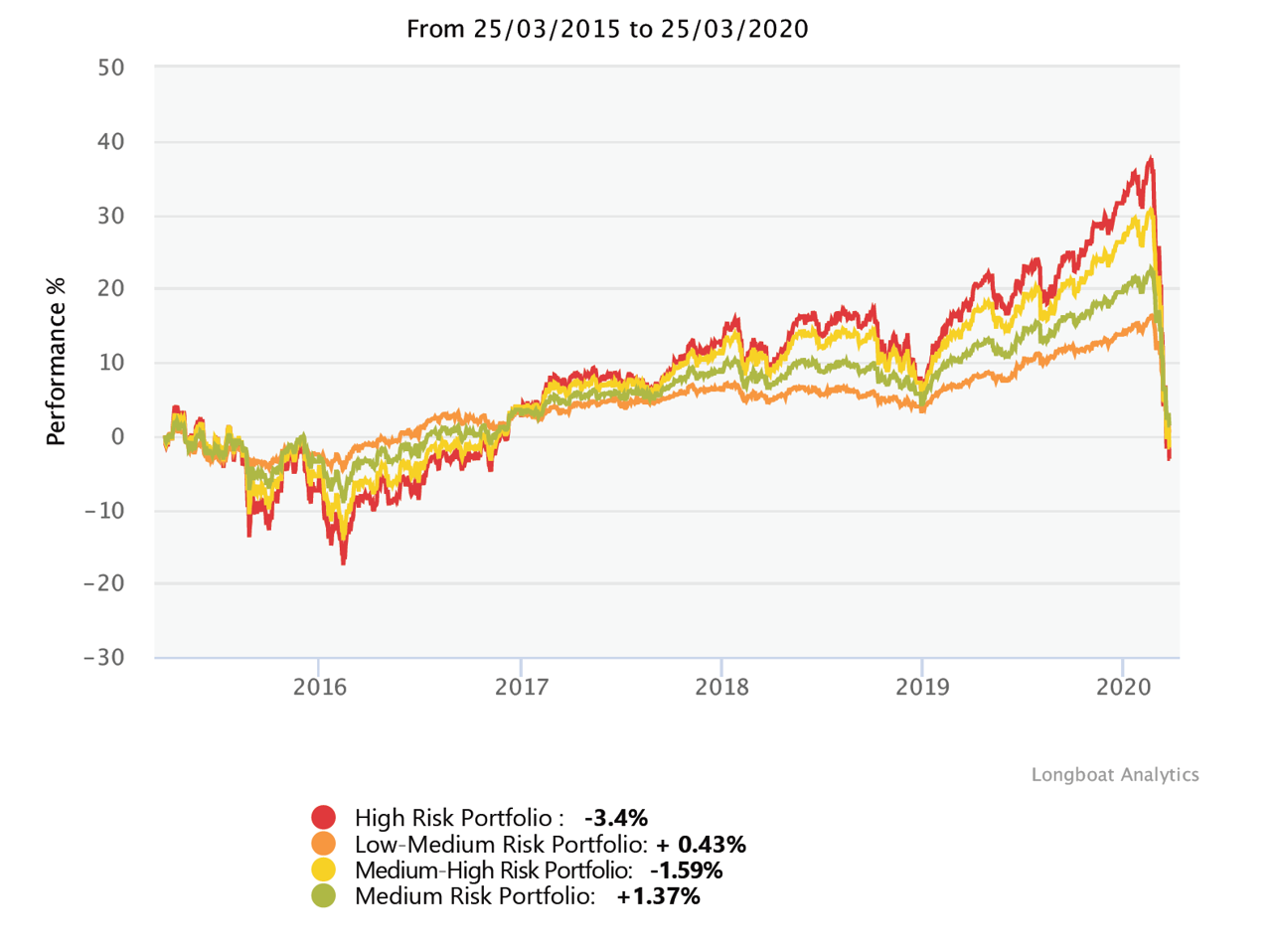

Your portfolio has thankfully performed fully in line with expectations. I’ve put together a chart (see Chart C below) outlining the performance of 4 different risk weighted portfolio’s over the past 5 years. The reason for 5 years is to demonstrate the medium-term performance of each portfolio.

Chart C. Typical Performance of Multi Asset Portfolio’s over past 5 years

As you see, the personalized ‘risk weighting’ of your portfolios has paid off. In simple terms if you have a high-risk portfolio then you’ve had a period of enormous gains but have suffered the worst loss but in real terms it’s still only -3.4% in 5 years. Stomach churning? Yes. But ‘total wipeout’? Absolutely not. In fact you’ll see that whilst the Lowest Risk portfolio has had a positive performance over that period it still lags the medium risk portfolio which, as expected, has performed the best as it has less money invested in Cash than a lower risk portfolio and Cash is yielding -0.8% pa at the moment!

3.) So what do we do now?

Only a fool calls the bottom of a market so I’m happy to say I’m not going to do that here. What I will do is state the obvious:

The one thing you don’t do is switch to Cash. It’s an awful asset, yielding -0.8% pa and, with the impending money printing being carried out by the European Central Bank, and indeed Central Banks all over Europe, it will remain that way for the foreseeable future. The only thing you’ll guarantee for yourself is a LOSS.

Therefore, the best advice is to do nothing with your existing portfolio. Here’s a link to a great article which expands on this but as I explained earlier, you are already in a risk weighted portfolio which will not have performed as terribly as the media will have told you.

I should state here that this isn’t the advice I’d give to everyone in all circumstances. If you’re investing directly in the stock market and have shares in a bad company which are performing terribly, they will continue to perform terribly and there’s zero value in holding on to them in the vain hope that they turn around. Best to cut your losses and re-invest in the best companies.

But this doesn’t apply to you as you are not invested in a single asset class containing only a small basket of shares. A typical medium-risk portfolio will be invested in 8 different asset classes, across 4000 companies in 82 countries so one company or even one asset class having a bad time of it will not take down your portfolio.

So that’s what we shouldn’t do. What should we do?

Depends! If you’ve made it this far and agree with most of what I’ve said, then you simply continue to save as you have been. Nothing should change.

However I will go out a limb and say that those of you who would now be prepared to take more risk, and are making regular premium contributions, should be considering the option to increase the risk on those contributions going forward for at least the next 12 months. It may sound counter intuitive but that way you will catch the downside (buying on the dip). It goes without saying that we don’t want anybody making such a decision without speaking to their advisor first, but I am happy to put it out there for people to consider. Anyone with the capacity to make a Lump Sum investment should choose a suitably risk weighted portfolio. It’s the same logic.

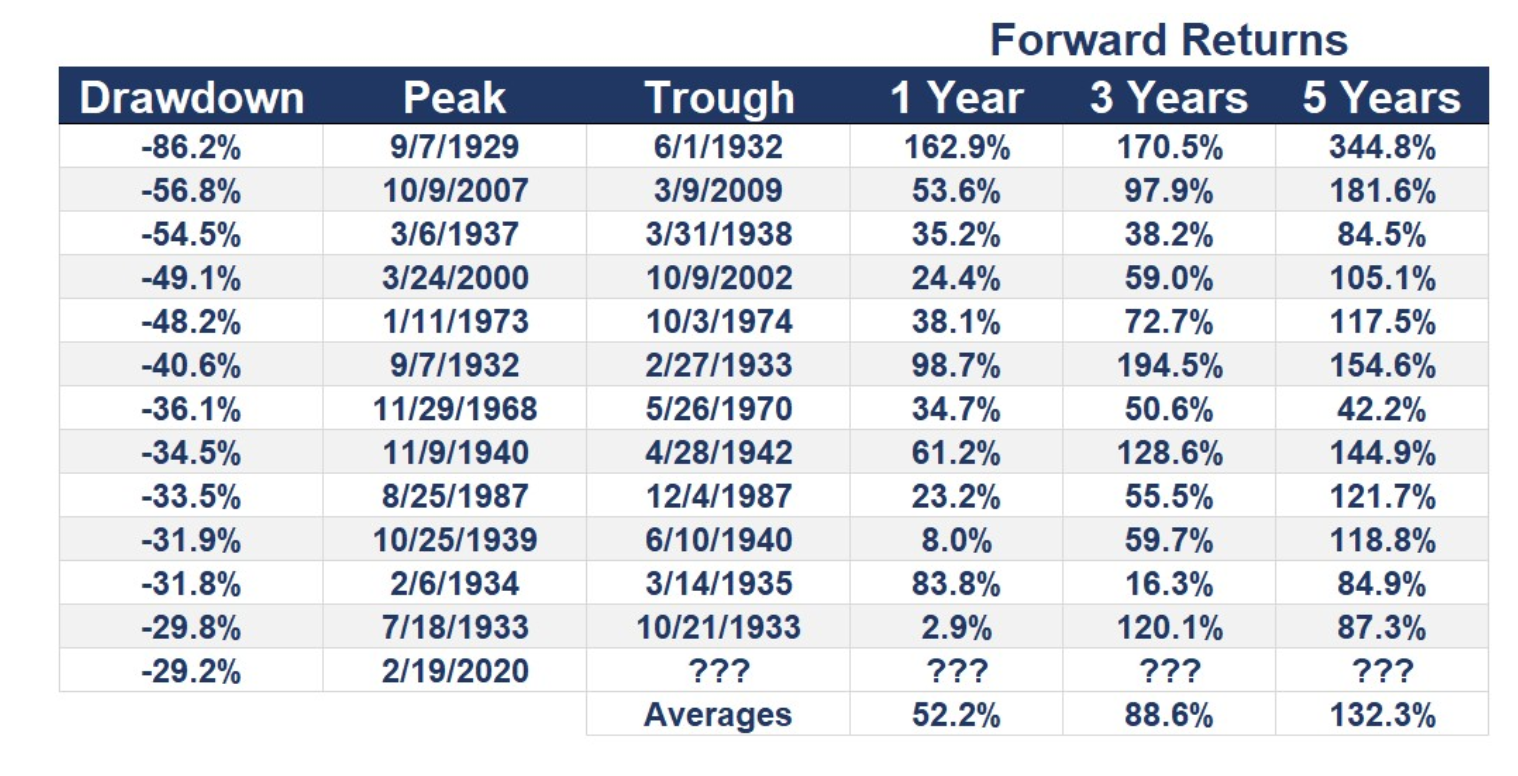

What gives me the confidence to say such things? Because it always has worked out. Warren Buffet famously said It’s not “Timing the market” but “Time In the market” however you must be able to psychologically withstand the volatility as it will get more volatile from here. It’s likely you won’t see the benefit of this for at least 5 years, but it will pay off. The chart below demonstrates the returns earned post every major stock market crash over the last 100 years and I see no reason why this time will be different.

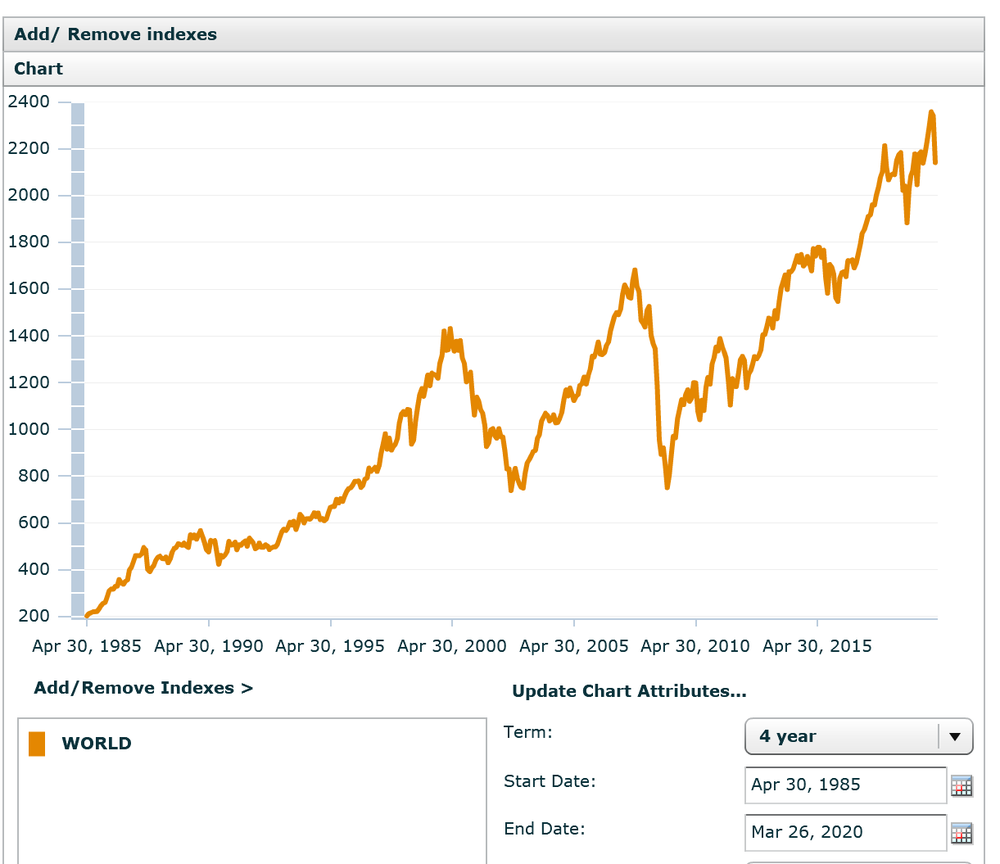

As for the benefits of long-term investing, I’ve included a chart below which shows the performance of the Global Stock market over the last 25 years. In real terms €200 invested in 1985 is worth €2,141 today, a 1071% return, despite the numerous corrections that have taken place over that time. “

In Conclusion

I hope this newsletter has helped give you a better understanding of the current situation in the investment world. Each investor is different, and we recognize that, so please get in touch with us if you have any questions about this or anything else that is happening to you financially.

But I think it’s fair to say that we’d all agree it’s not the most important issue facing us right now. Never has the adage that ‘Your health is your wealth’ been more appropriate.

Please stay safe, continue to follow the advice of the HSE and WHO, and we look forward to meeting you (in person!) again.

Robert Whelan, Managing Director, Rockwell Finanical

Tel: 01-2966120

Got a Question?

Let us help

-

Icon Accounting, Columba House, Airside,

Swords, Co. Dublin, Ireland, K67 R2Y9